The Debt Trap That Nobody's Escaping

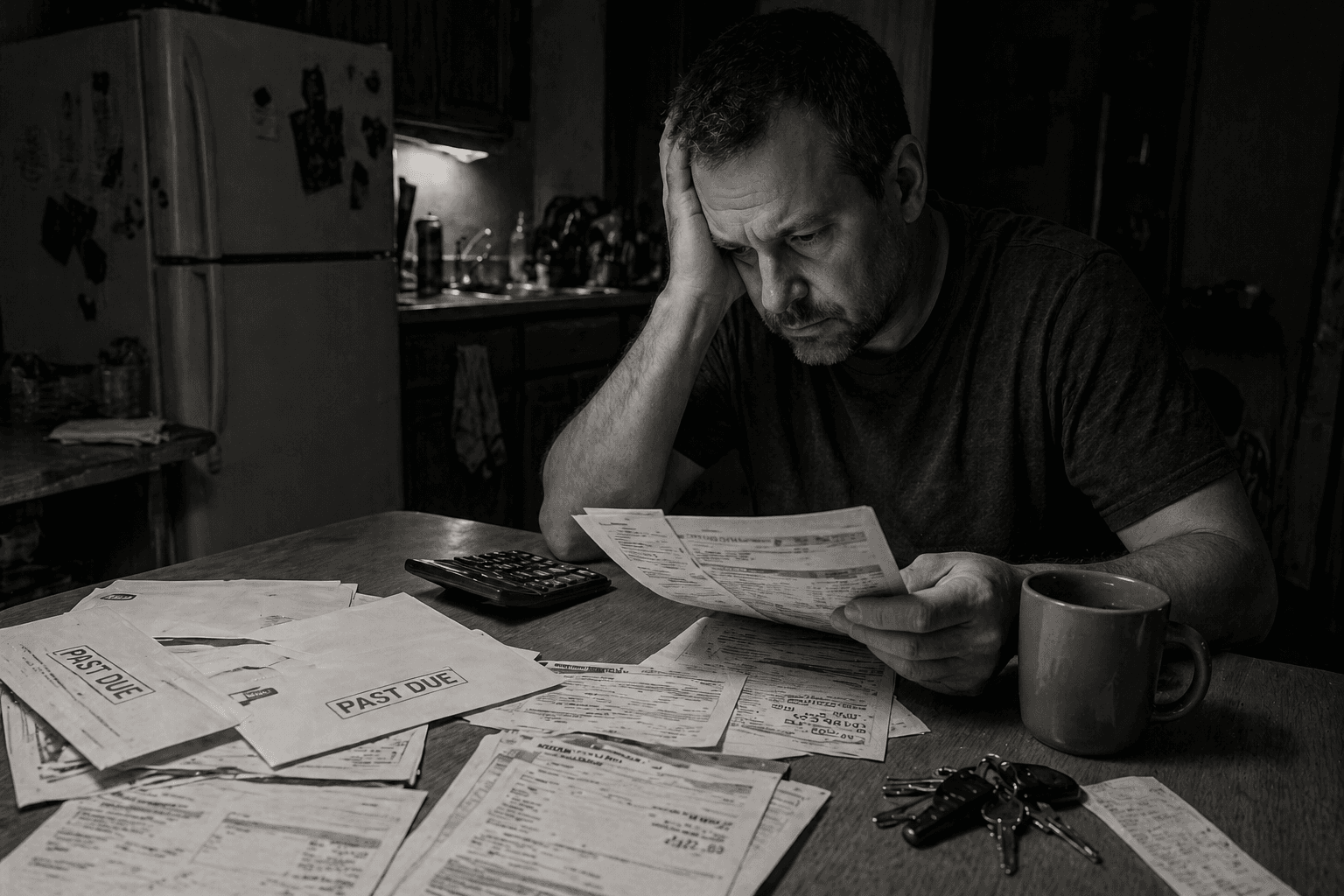

$100,000 average household debt. 11% of monthly income just servicing it. Not paying it down — just keeping the lights on.

One hundred thousand dollars. That's the average American household debt. Nearly half of Americans say their credit card debt is about to increase. The average revolving balance is $6,500. And Americans spend 11% of their monthly income just servicing debt. Not paying it down. Just keeping the lights on.

Vacation spending is down. Dining is down. Everyone except the top 5% and baby boomers is spending less. And it's not a choice. They can't afford to spend. That's the distinction.

A lot of this traces back to the car industry. Transportation expenses are a debt trap. Car payments average $767 per month for new vehicles, $537 for used. Twenty percent of new car buyers now pay over $1,000 per month. Insurance, maintenance, fuel: it compounds. The car industry handcuffed people into terrible financial conditions. And then you layer on income disparity, economic uncertainty, job transitions, and technology innovation — everyone has the same problem but nobody's talking about it.

For low-income households, transportation consumes 32% of their income. For high-income households, it's 9.6%. The gap exposes the inequality.

Here's what's encouraging: individuals have never had more power over their finances. Never.

The tools exist. Financial education exists. The ability to understand systems exists. The barrier isn't knowledge anymore. It's action.

Personal financial literacy is the leg up. Understanding how debt works, how interest compounds, how minimum payments trap you — that's the attack vector. You don't need to be rich to fix debt. You need to understand it.